In the realm of financial decision-making, understanding and managing risk is fundamental to preserving capital and ensuring long-term stability. Risk calibration, the process of adjusting investment strategies and exposure to potential losses, is a cornerstone of sound financial practice. Without proper risk calibration, investors and institutions are prone to overexposure, which can lead to substantial losses, eroded trust, and compromised financial objectives. By carefully evaluating risk tolerance, market conditions, and portfolio composition, individuals and organizations can better safeguard their assets while maintaining opportunities for growth.

The first principle in risk calibration involves assessing one’s capacity to withstand losses. Each investor or firm has a unique risk profile influenced by financial goals, time horizons, liquidity needs, and psychological resilience. For instance, an individual nearing retirement may prioritize capital preservation over aggressive growth, favoring low-volatility assets. Conversely, a young investor with a long investment horizon might tolerate higher volatility for the potential of greater returns. Recognizing these limits allows decision-makers to tailor their exposure, preventing scenarios where losses exceed acceptable thresholds and jeopardize overall financial health.

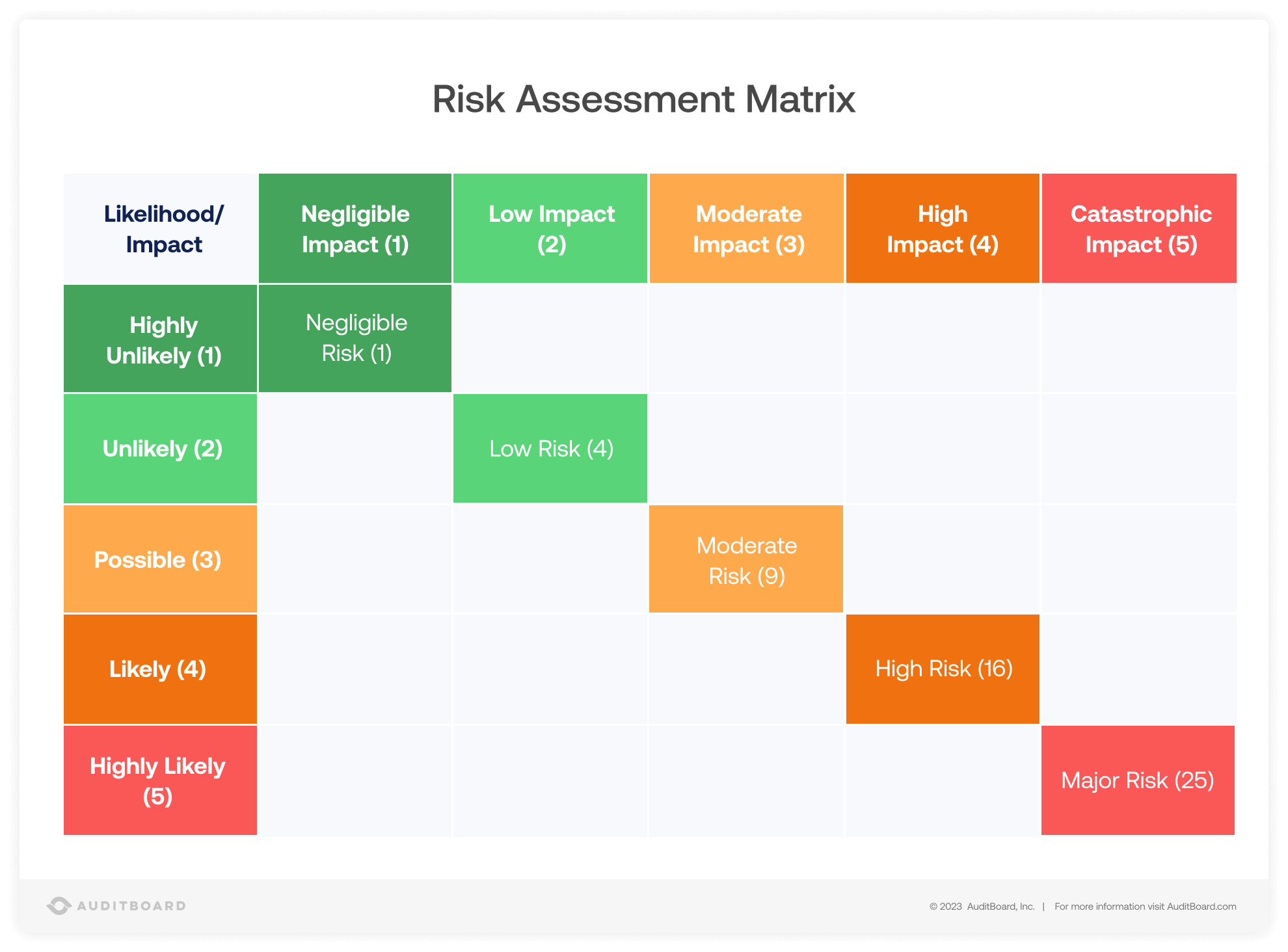

Risk calibration also relies on understanding the nature and likelihood of different types of risk. Market risk, credit risk, liquidity risk, and operational risk each present unique challenges. Market risk arises from fluctuations in asset prices due to economic, political, or social factors, and can significantly impact portfolios if not managed carefully. Credit risk involves the potential default of borrowers or counterparties, whereas liquidity risk refers to the difficulty of converting assets into cash without significant loss. Operational risk encompasses internal failures, from human error to system malfunctions, that can unexpectedly affect outcomes. By evaluating these dimensions systematically, investors can implement protective measures, such as diversification, hedging, and contingency planning.

Diversification is a key tool in calibrating risk. By spreading investments across different asset classes, industries, or geographic regions, the impact of any single adverse event is mitigated. For example, holding both equities and fixed-income instruments reduces exposure to equity market volatility. Similarly, investing across multiple sectors ensures that underperformance in one area does not devastate the entire portfolio. Diversification, when executed thoughtfully, transforms unpredictable fluctuations into manageable variations, helping preserve capital while still capturing opportunities for growth.

Another essential aspect of risk calibration is position sizing. This involves determining the appropriate amount of capital to allocate to each investment relative to its risk profile. Oversized positions in volatile assets can magnify losses, whereas undersized positions may limit returns unnecessarily. By carefully calibrating position sizes according to volatility, correlation, and individual risk tolerance, investors achieve a balance that maintains portfolio stability. This discipline prevents emotional decision-making and reduces the likelihood of catastrophic losses during periods of market stress.

Risk calibration is not static; it requires continuous monitoring and adjustment. Markets evolve, economic conditions shift, and individual circumstances change. A portfolio that was suitably balanced six months ago may now carry unintended exposures due to market trends or new information. Regular reassessment allows investors to recalibrate risk exposure, rebalancing portfolios, adjusting stop-loss thresholds, or modifying hedging strategies. This dynamic approach ensures that capital preservation is maintained even as external conditions fluctuate, preventing complacency and reactive decision-making.

Stress testing and scenario analysis are practical methods to enhance risk calibration. By modeling the potential impact of extreme market events, investors can identify vulnerabilities and take proactive measures. Stress tests may simulate interest rate shocks, currency fluctuations, or sudden declines in asset values, providing insights into portfolio resilience. Scenario analysis goes further by considering combinations of events, helping decision-makers anticipate complex interactions and cascading effects. These exercises illuminate potential weaknesses, allowing for targeted adjustments that safeguard capital under adverse conditions.

Psychological discipline is another critical element in effective risk calibration. Human behavior often introduces bias, overconfidence, or panic, leading to poor decisions that erode capital. A calibrated approach encourages adherence to predetermined strategies, risk limits, and contingency plans, mitigating impulsive actions driven by fear or greed. By cultivating patience and a long-term perspective, investors resist the temptation to chase short-term gains or abandon strategies at the first sign of volatility. This mental framework complements technical measures, ensuring that risk management is comprehensive and sustainable.

Incorporating technological tools further enhances the calibration of risk. Advanced analytics, real-time monitoring systems, and algorithmic models provide quantitative assessments of exposure, correlation, and volatility. These tools enable more precise adjustments, informed decision-making, and rapid response to emerging threats. While technology is not a substitute for judgment, it amplifies the ability to manage complex portfolios, identify anomalies, and implement protective measures efficiently. The integration of analytics with human oversight ensures that risk is calibrated with both precision and context, reducing the likelihood of unforeseen capital erosion.

Ultimately, risk calibration preserves capital by transforming uncertainty into a manageable element of the investment process. It aligns strategy with capacity, integrates protective measures, and incorporates continuous oversight to mitigate potential losses. By balancing the pursuit of returns with the preservation of principal, investors build resilience into their financial structures. This approach does not eliminate risk, but it ensures that risk is intentional, measured, and aligned with objectives. Capital preservation, in turn, provides the foundation for long-term growth, stability, and confidence in financial decision-making.

The practice of risk calibration is not limited to professional investors; it applies to anyone managing financial resources, from individuals to corporations. Understanding exposure, employing diversification, sizing positions appropriately, and maintaining discipline are universal principles. Whether navigating volatile markets, uncertain economic conditions, or personal financial goals, calibrated risk management preserves the integrity of capital, enabling opportunities for sustained wealth accumulation. In an environment defined by unpredictability, the ability to measure, adjust, and respond to risk is the most reliable safeguard for enduring financial success.

By consistently applying these principles, investors protect their capital from unnecessary losses while positioning themselves to benefit from opportunities as they arise. Risk calibration instills a mindset of prudence and foresight, ensuring that decisions are neither reckless nor reactive. Through careful analysis, disciplined execution, and ongoing evaluation, capital is preserved, confidence is maintained, and long-term objectives remain achievable, regardless of market turbulence or external uncertainties.

This philosophy of measured exposure and proactive management underscores the importance of risk calibration as a cornerstone of financial prudence. It affirms that success in investment is not merely about seeking gains, but about protecting what has been accumulated, ensuring that resources remain intact for future growth. By embracing risk calibration, investors cultivate resilience, stability, and the capacity to navigate uncertainty without compromising their core financial foundation.

Leave a Reply